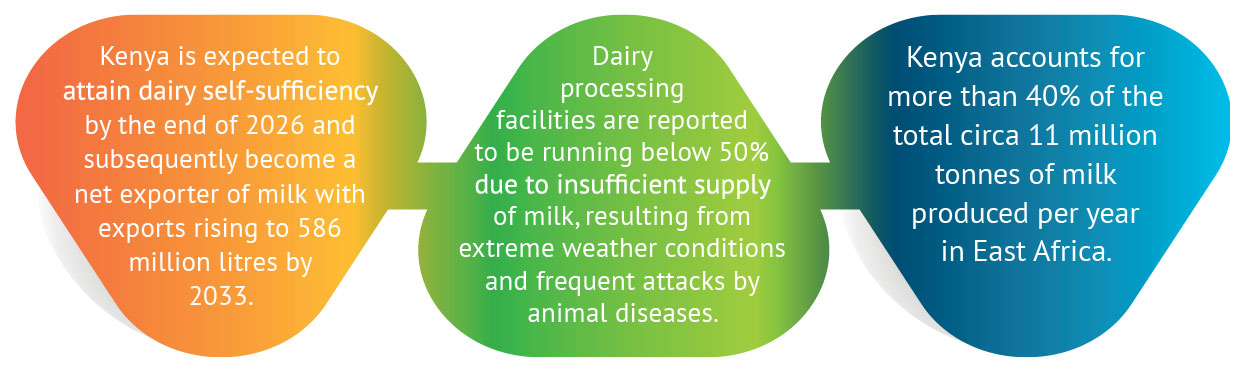

In 2024, global milk production increased by 1.1% to approximately 950 million metric tonnes, of which 60 million metric tonnes came from Africa. Egypt, Kenya, and Tanzania were the main producers, accounting for 7.5, 6.6, and 5 million metric tonnes, respectively. In the near term, Africa is expected to experience strong production growth, supported by a larger herd population and increased yields per animal. However, the total consumption is projected to grow faster than production, necessitating an increase in imports.

The Kenyan dairy Industry accounts for approximately 17% of the agricultural GDP and 4.2% of the national GDP and is on an upward trajectory with an estimated growth rate of 3%-4%[1] annually. In H1 2025, formal milk intakes surged to 522.6 million litres, representing a year-on-year growth of 19% from 438.9 million litres[2]. The Industry growth is, however, constrained by low productivity levels, high production costs, a large informal sector, uncoordinated disease management systems and limited skills and knowledge. Milk production in Kenya is overwhelmingly smallholder-dominated, with farmers owning between one and five cows contributing approximately 80% of the total national milk output[3]. Kenya’s current per capita milk consumption estimated at 110 litres per annum is projected to reach 220 litres by 2030[4]. Looking ahead, Agusto & Co. anticipates sustained growth in the Industry, driven by robust animal health management, adoption of enhanced animal husbandry practices and a shift towards value addition, in line with the Kenya Dairy Board’s strategic plan that aims to achieve a 20% annual growth in milk production and value addition.

The 2025 Kenya Agriculture (Dairy) Industry Risk Report captures the following: