According to the 2026 Economic Survey by the Kenya National Bureau of Statistics (KNBS), the construction industry rebounded in 2025, posting real growth of about 6.8% driven by increased civil works, particularly the construction and maintenance of roads—alongside a pick-up in residential building activity in major urban centres. The rebound was further evidenced by a 20.3% increase in cement consumption, a 50.7% rise in the volume of imported iron and steel, and a 45.5% year-on-year increase in credit extended to construction enterprises. In addition, the construction industry accounted for roughly 6.5% of Kenya’s Gross Domestic Product (GDP), equivalent to about KSh 1.14 trillion in nominal terms, underscoring the Industry’s macroeconomic importance.

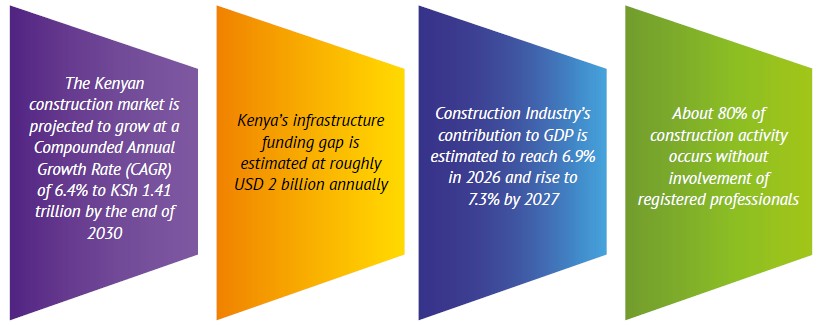

The Kenyan construction industry spans residential and commercial buildings, industrial facilities and a broad range of civil and transport infrastructure, with industry activity shaped by the interplay between public works aligned with national and county development agendas and private-sector construction responding to market demand for both affordable and premium property. Over the last five years (2021-2025), the Industry has enjoyed sustained growth on the back of increased government investment in transport and energy infrastructure, as well as rising demand for residential units driven by population growth. Kenya’s infrastructure funding gap is estimated at roughly USD 2 billion annually[2]. To close this gap, the government is shifting towards relying more on dedicated levies and funds, such as the Roads Maintenance Levy Fund and the Housing Levy, as well as public-private partnerships (PPPs) and an evolving KSh 5 trillion National Infrastructure Fund.

Looking ahead, Agusto & Co. projects that Industry output will grow by circa 7.3% in 2026, on the back of sustained public infrastructure investment, rising private and foreign investment in construction, increased investment in green buildings and an expanding pipeline of PPP projects. In addition, the gradual adoption of technology‑driven construction methods to enhance efficiency and quality will further support this growth. Nonetheless, the Industry faces persistent challenges, including declining development approvals in some key counties, weak compliance with building standards, slow uptake of professional services, rising construction costs, high dependence on imports, uneven implementation of spatial and development plans, limited adoption of digital processes and regulatory inconsistencies[3].

The 2026 Kenya Construction Industry Risk Report captures the following: